How Maybern Empowers Fund CFOs to Meet ILPA Principles

Private equity firms face growing operational complexity driven by larger fund sizes, diverse investment strategies, and heightened regulatory scrutiny. Simultaneously, the Institutional Limited Partners Association (ILPA) has raised the bar for transparency, fund governance, and alignment through its Principles 3.0 framework. This piece breaks out the pain points around transparency & reporting in ILPA compliance, and how to address key operational challenges.

Private equity funds are getting harder to administer. McKinsey's Global Private Markets Report 2025 documents the shift to more products, more vehicles, more intensive client servicing, and narrowing margins. LPs are also demanding more transparency, and in January 2025, ILPA released its updated Reporting Template for implementation in Q1 2026. Fund CFOs increasingly see a gap in what their current systems can handle in the face of these requirements.

Fund Complexity is Accelerating

Firms handle more data today than five years ago. Data flows from portfolio companies, administrators, custodians, and internal systems. Without a unified architecture, finance teams spend hours reconciling spreadsheets and chasing discrepancies. Manual data entry introduces potential errors. When data exists in multiple disconnected systems, the reconciliation burden grows with each new fund and subsequent closing.

The scale has also increased. The median PE fund size reached a record $183 million in Q3 2025, with per-firm AUM also growing larger. As fund sizes grow, finance teams must process more transactions, capital calls, and distributions.

Managers are also expanding across asset classes and vehicle types. GPs that once invested in distinct verticals now invest at the intersection of different themes - energy and digital assets for data centers, for example. Private credit, infrastructure, and real estate strategies increasingly sit alongside traditional buyout funds within the same organization. Each has distinct accounting requirements, waterfall structures, and reporting standards.

New fund structures also add complexity. GPs are setting up continuation vehicles and sourcing capital through open-end and semi-open-end funds to address LP liquidity demands. In the U.S., evergreen and semi-liquid vehicles grew to $400 billion in AUM and attracted $64 billion in inflows in 2024. Each structure has distinct NAV calculation methodologies, redemption mechanics, and investor reporting requirements that legacy systems cannot handle.

As fundraising becomes more competitive, managers grant investor-specific waterfall terms, fee waivers, and excused investor provisions. Each side letter adds another variable to track across every capital call and distribution.

Finally, LPs also expect faster turnaround on ad-hoc requests for capital account balances, transaction histories, and custom performance cuts. Finance teams field these queries while managing quarterly close cycles. The workload increases as investor bases grow and diversify across vehicle types. Formal disclosure standards add further pressure, as described in the next section.

Transparency and Reporting: Meeting ILPA Standards

ILPA’s updated Reporting Template codified what sophisticated LPs already expected: full transparency into calculations and reporting that stands up to regulatory scrutiny. The updated Reporting Template (v. 2.0) is the most significant change to private equity reporting standards since 2016.

The new standards require granularity in three key areas:

- Waterfall Logic: Funds must track every input and output, not just total distribution amounts. If an LP requests documentation of their distribution calculation, the response must be verifiable against LPA provisions.

- Expense Disclosures: Firms must break out internal chargebacks to identify expenses allocated to GPs or related persons. External partnership expenses must align with general ledger categories. ILPA has removed the ability to modify the template—repurposing or reordering line items is no longer permitted.

- Performance Metrics: The new Performance Template captures metrics alongside contributions and distributions. Standardized reporting now covers IRR, TVPI, and MOIC with designated breakouts for gross and net figures.

How Technology Can Deliver What the Fund CFO Needs

Maybern’s platform addresses these operational and compliance challenges by replacing fragile manual processes with precision.

1. Traceable Waterfall Calculations The system handles complex waterfall calculations with full transparency. Unlike spreadsheet models where upstream errors cascade through subsequent tiers, Maybern validates calculation logic against LPA provisions and prevents illogical configurations. The architecture supports investor-specific terms—side letters, fee waivers, and unique preferred returns—without requiring parallel manual processes.

2. Unified Data Architecture Maybern consolidates information into a single source of truth, eliminating the reconciliation burden. When subsequent closings occur, the system automatically tracks which capital applies to which time period for preferred return purposes.

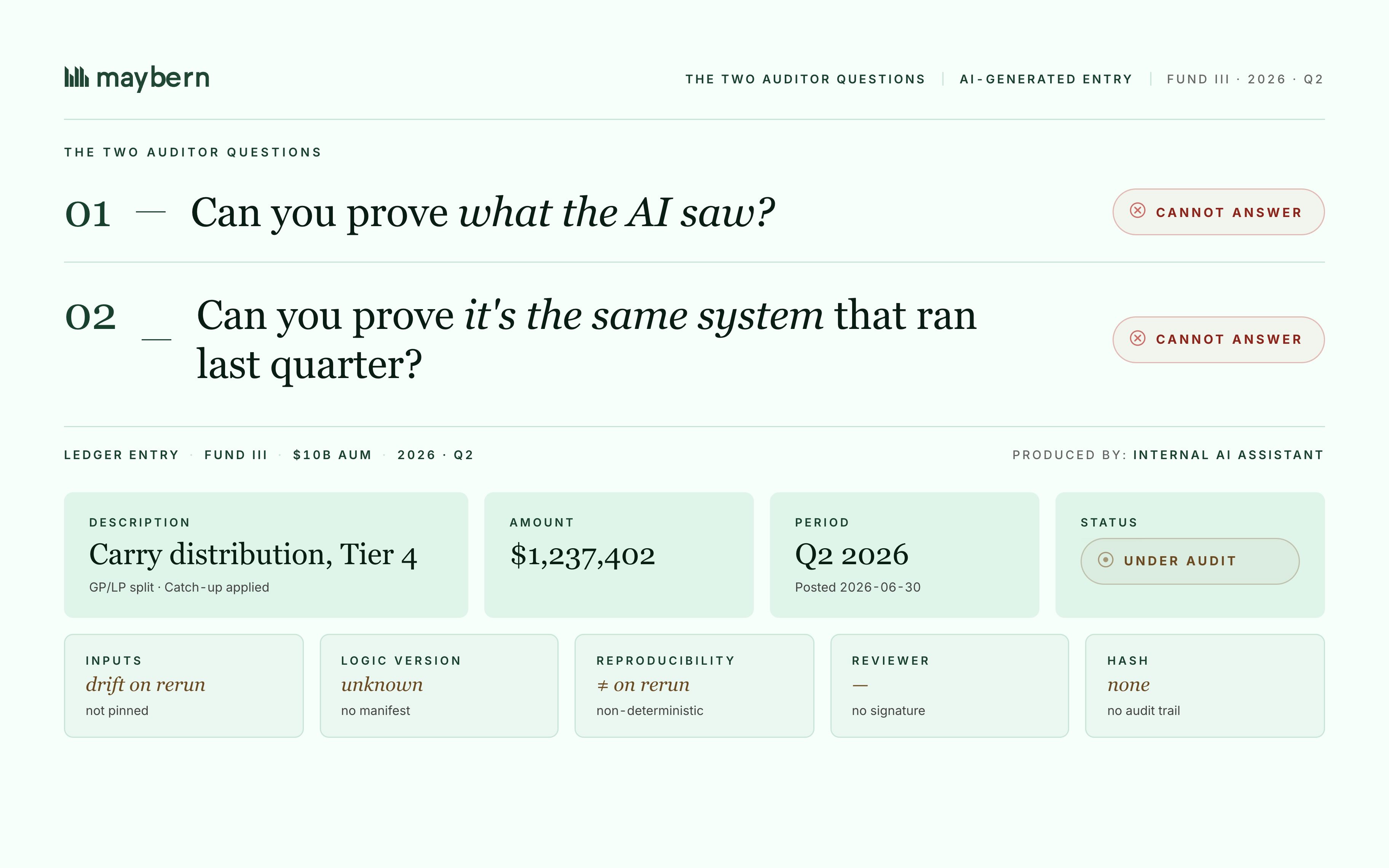

3. Automated Reporting & Audit Trails The platform automates reporting across fees, expenses, and performance metrics. Rather than assembling quarterly reports manually, fund CFOs generate disclosures that meet ILPA’s granularity requirements directly from the system. Built-in audit trails record every change, allowing teams to instantly identify if a distribution shift resulted from corrected formulas, updated inputs, or calculation errors.

Conclusion

Private equity's operational demands have outpaced the manual processes most firms rely on. Without purpose-built infrastructure, finance teams will remain stuck reconciling spreadsheets, chasing discrepancies across disconnected systems, and fielding LP requests—a workload that outpaces headcount as fund size and complexity increases.

Technology platforms help close this gap by replacing fragile manual processes with traceable waterfall calculations, unified data architecture, and automated reporting that meets ILPA's requirements out of the box. The firms best positioned for the next decade have already moved from spreadsheet-based workflows to platforms that handle complexity programmatically, freeing finance teams to focus on strategic work rather than data wrangling. With private markets projected to grow to $32 trillion of AUM by 2030, fund CFOs need infrastructure that scales with them, not against them.

Frequently asked questions

Quick reference for this topic.

01

02

03

04

05

Recommended Content

AI Sovereignty Is the Future of Fund Alpha

The Maybern MCP is Live

Why Internally-Built AI Fails Fund Accounting Audits