What a Fund Performance Layer Solves That Asset-Level Tools Cannot

A portfolio manager at a private capital firm needs to answer a series of questions that span investment decisions, LP reporting, and fund strategy. Most of those questions today get answered through manual aggregation across fund administrator statements, general ledger entries, asset-level performance tools, and Excel models built over years. By the time the answer arrives, the underlying data is 60 to 90 days old. The question is whether the right architecture can change that, and what the architecture actually needs to be.

- Performance data fragmentation is the silent tax on private market returns. By the time finance teams reconcile quarterly statements, GL entries, and individual deal trackers, the data is already 60 to 90 days old.

- Different team members on the same fund often use different calculation conventions. One calculates returns on committed capital, another on invested. The blended portfolio view that should answer the IC's question can't be produced consistently because the inputs disagree.

- Scenario modeling rarely happens because the manual effort isn't worth it. The result: exit-timing and valuation-shift questions go unanswered before the decisions that depend on them get made.

- Custom LP reporting requests (returns by sector, geography, vintage, hold period) trigger one-off manual work each time. During fundraising peaks, when those requests cluster, finance teams fall behind.

- A performance book of record with transaction-level capture solves the aggregation problem at the architecture level. Blended returns across funds, equalized versus actual investor returns, and custom metric calculations all become queries instead of projects.

The Category Structure That Matters

Most performance data conversations conflate three distinct categories of tools that solve three different problems.

Asset-level performance management. Tools like iLevel, Chronograph, and 73 Strings centralize the operational and valuation data for individual portfolio companies. They are purpose-built for the asset management function: collecting financials from portfolio company finance teams, normalizing the data, running valuation models, and producing GP-grade reports on deal-level performance. They are the system of record for the operational story of each investment.

Fund accounting. Fund administrators and accounting platforms produce the books of the fund itself: capital calls, distributions, expense allocations, and the partnership tax records that drive K-1 issuance. They answer the question "what did the fund do this quarter" at the entity level.

Fund-level and investor-level performance. This is the layer where asset-level performance, fund accounting, and LP-specific terms come together. It produces the answers to questions like "what is this LP's blended return across our three vintages with their specific fee tier" or "what is the fund's projected TVPI under three exit scenarios for the remaining portfolio companies." Most firms today produce this layer in Excel. Asset-level tools are not built for it, and fund accounting platforms do not have the LP-specific or scenario logic to support it.

The performance book of record sits in the third category. It connects to the asset-level tools and the fund accounting system, and produces the fund and investor-level views those tools cannot.

What Changes With A Performance Book of Record

Three changes follow from putting the fund and investor-level performance layer on its own architecture rather than in Excel.

The first is consolidation. When an LP participates across multiple vintage funds with different fee tiers, calculating their blended return manually requires reconciling capital account statements from each fund, applying each fund's fee economics correctly, and resolving any discrepancies between the GL and the admin's records. In a book of record with transaction-level capture, the blended return is a query that completes in seconds and traces back to the underlying capital events.

The second is custom segmentation. LP reporting requests for sector-level, geography-level, vintage-level, or hold-period-level performance breakdowns currently trigger one-off manual analysis. In a structured performance layer, these become standing reports rather than projects. The marginal cost of the second sovereign wealth LP's bespoke energy-sector report drops to zero.

The third is natural-language querying. Consider one example. "What is our aggregate TVPI across deals in the energy sector closed since 2021, weighted by check size and excluding bridge financings?" In a spreadsheet workflow, this question takes a senior analyst a full day to answer. Most of that time goes to data assembly, not to the question itself. In a performance book of record with natural-language access to the underlying data, the same question completes in seconds, with traceable lineage from the answer back to the individual transactions.

The Scenario Modeling Shift

Scenario modeling for exit timing and valuation shifts is the part of portfolio management that most firms intend to do and most do not actually do. The reason is operational, not philosophical.

Building a scenario in Excel requires constructing a one-off model with assumptions for each remaining portfolio company, flowing them through the fund's specific waterfall structure, and projecting management fees, carried interest, and LP distributions under each scenario. The model takes a senior analyst three days to build and is fragile against any change in assumption. After the model produces its answer once, it gets archived and not reused, because updating it for new assumptions costs nearly as much as building it.

The result is that exit-timing decisions on individual deals usually get made on instinct rather than on modeled tradeoffs. The question "should we exit deal A in Q2 or hold for a year" gets answered without the model that would show how the timing affects fund-level returns, the GP's carry trajectory, or specific LP outcomes.

When scenario modeling is architectural rather than manual, the conversation changes. The IC can compare three exit-timing options for a deal in real time during the meeting. The fund can produce projection updates monthly rather than annually. The CFO can model the impact of LP segment-level fee waivers before agreeing to side-letter terms.

The Honest Tension

The harder question is whether portfolio managers actually use the recovered time well.

The firms we work with have applied it in two directions. The first is scenario modeling on exit timing, which produces measurably better outcomes when the team trusts the model enough to act on it. The second is LP segment-level reporting that has won allocations from institutional investors who require it as a condition of due diligence.

We have also seen firms recover the operational time and dissolve it into more meetings. The infrastructure matters. The discipline to redeploy the recovered time toward strategic work matters more, and that is not a technology problem.

Frequently asked questions

Quick reference for this topic.

01What is a performance book of record in private capital?

A performance book of record is a single governed source for fund and investor-level performance data, distinct from asset-level performance tools that track portfolio companies and fund administrators that produce the fund's books. It captures every capital call, distribution, valuation, and allocation at the transaction level, and produces blended returns, scenario projections, and custom segment reporting as queries rather than manual analyses.

02How do iLevel, Chronograph, and 73 Strings fit with a fund performance platform?

Those tools are purpose-built for asset-level performance management. They centralize portfolio company financials, run valuations, and produce deal-level performance views. They do not roll up to fund-level or investor-level performance with LP-specific fee terms. A fund performance platform sits on top of those tools, takes their asset-level outputs as one input, and produces the fund and LP-level views the asset-level tools cannot.

03How do you calculate blended IRR for an LP who invested across three vintages with different fee tiers?

The math requires reconciling each fund's capital account for that LP, applying each fund's specific fee economics, and aggregating cash flows on a single timeline. In Excel, this is a half-day project per LP per request. In a performance book of record with transaction-level capture and LP-specific terms encoded as rules, the calculation is a query that completes in seconds and traces back to the underlying transactions.

04What does it cost operationally to support custom LP segment reporting on demand?

For firms running on Excel, each custom segment request (returns by sector, geography, vintage, or hold period) requires a senior analyst to build a bespoke pull and analysis, typically four to eight hours per request. During fundraising peaks the requests cluster, and firms either delay responses, which costs LP credibility, or hire temporary support, which costs margin. With a performance book of record, the same requests become standing queries with zero marginal effort per LP.

05When does scenario modeling stop being a one-off Excel build?

When scenario inputs, the fund's waterfall logic, and LP-specific terms all live in a system that can re-run projections automatically against new assumptions. The signal that a firm is past the one-off stage is that scenario projections update monthly without analyst time, and the investment committee can compare scenarios in real time during the meeting rather than waiting for a follow-up.

Recommended Content

AI Sovereignty Is the Future of Fund Alpha

The Maybern MCP is Live

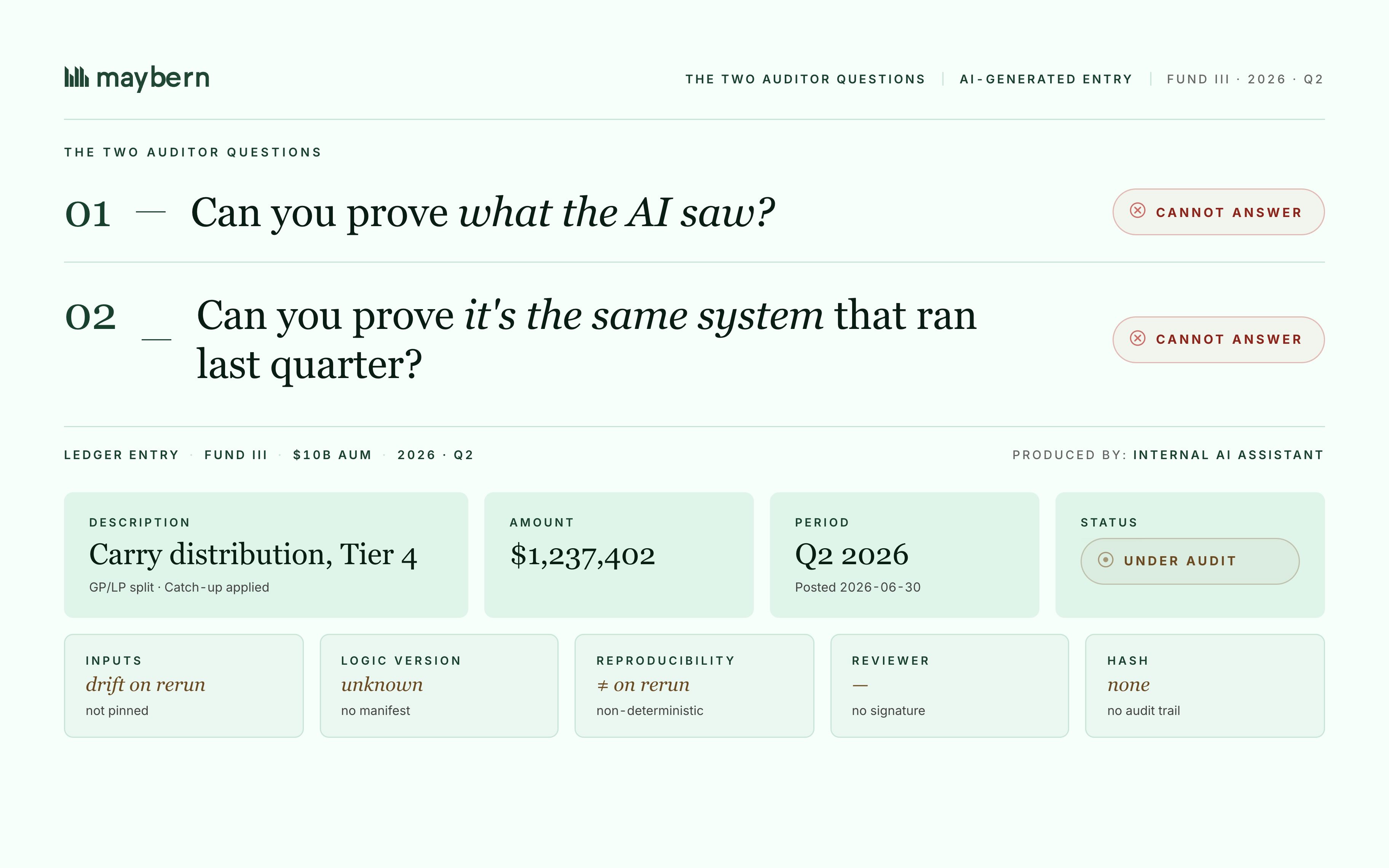

Why Internally-Built AI Fails Fund Accounting Audits