Fund Structure Complexity as a Strategic Advantage

Parallel vehicles, co-invest, AIVs, side letters — the structural complexity that defines modern private funds is also the operational burden that defines them. The funds that treat complexity as a strategic advantage — saying yes to bespoke LP terms others decline — share one thing in common: they manage the obligations in code, not in spreadsheets.

- Feeders, blockers, and co-investment vehicles let LPs structure capital the way they need. Each layer is an operational tax on fund finance teams using Excel.

- Manual reconciliation across entities scales linearly with fund growth. Limited visibility across the full structure means problems compound across entities before anyone notices.

- Funds that treat structural complexity as a strategic advantage share one trait: they manage obligations in code, not spreadsheets, which lets them accept LP requests competitors must decline.

- LP satisfaction depends on response speed to entity-specific questions. Spreadsheet-based reporting introduces lag and error precisely when LPs are evaluating their next commitment.

- Custom code workarounds and bolted-on tools don't solve multi-entity complexity. They delay the moment when complexity becomes a growth ceiling.

Private fund managers face mounting complexity as limited partner demands and tax requirements drive the need for increasingly sophisticated fund structures. Firms managing these structures face a critical choice: struggle with error-prone manual processes or embrace purpose-built technology solutions.

While others offer workarounds or complex custom code for multi-entity funds, Maybern is the only solution purpose-built to handle the intricacies of private fund structures without compromise—delivering a centralized, integrated, and flexible platform that scales with your complexity.

Complete Visibility, Complete Control

Operational complexity in private equity firms increases dramatically as assets under management grow. This complexity is especially evident in the management of multi-entity structures including feeders, blockers, and co-investment vehicles.

For fund finance teams, managing these structures traditionally means:

- Maintaining countless Excel spreadsheets

- Manual reconciliation across entities

- High risk of errors and reporting delays

- Limited visibility into the complete fund structure

These challenges aren't just operational inconveniences; they represent real barriers to strategic growth and LP satisfaction. Maybern's solution to complex fund structures addresses these challenges head-on by providing a unified platform where fund structures can be modeled, managed, and monitored with precision and ease.

Frequently asked questions

Quick reference for this topic.

01Why have fund structures grown more complex over the past decade?

Three drivers compound. LPs negotiate more bespoke terms as they consolidate AUM and gain leverage, generating per-LP side letters that require operational support. Cross-border investment requires parallel vehicles, AIVs, and blockers to manage tax treatment for different LP types. And regulatory pressure pushes funds toward structural disclosure that incentivizes documenting complexity rather than hiding it.

02Is fund structure complexity a cost or an advantage?

It depends on whether the GP can operate it. Complexity that the GP can configure and explain to LPs is a moat: it lets the manager accept commitments from LP types competitors cannot serve, structure around regulatory regimes competitors cannot navigate, and offer side-letter terms competitors cannot administer. Complexity the GP cannot operate is a cost: it generates errors, slows close, and creates LP disputes that erode credibility.

03What structural features become competitive advantage with the right infrastructure?

Master-feeder structures that accommodate tax-exempt and foreign LPs in the same fund. Parallel funds that segregate strategies without fragmenting the GP's investment selection. AIVs that allow specific deals to be held outside the main fund for tax or regulatory reasons. Fee tier structures that let the GP differentiate pricing without breaking the fund's allocation math. Each of these is operationally costly without governed infrastructure and competitively neutral with it.

04How do GPs decide which structural features are worth the operational cost?

The decision turns on three questions. Does the structure expand the addressable LP base? Does it enable tax or regulatory positioning competitors cannot match? Does it support a strategy that needs the structure to function? Structural features that fail all three are operational drag. Features that pass even one become moat candidates if the GP can operate them at acceptable cost.

05What does fund structure innovation look like over the next five years?

The clear direction is continuous fund finance: structures that allow ongoing LP turnover, real-time capital activity, and modular fund composition rather than the closed-end, fixed-term, fixed-structure model that has dominated since the 1980s. The funds that execute this transition first will gain access to LP capital that today cannot accept the illiquidity of traditional closed-end structures. The operational infrastructure to support continuous fund finance is the prerequisite, not the consequence.

Recommended Content

AI Sovereignty Is the Future of Fund Alpha

The Maybern MCP is Live

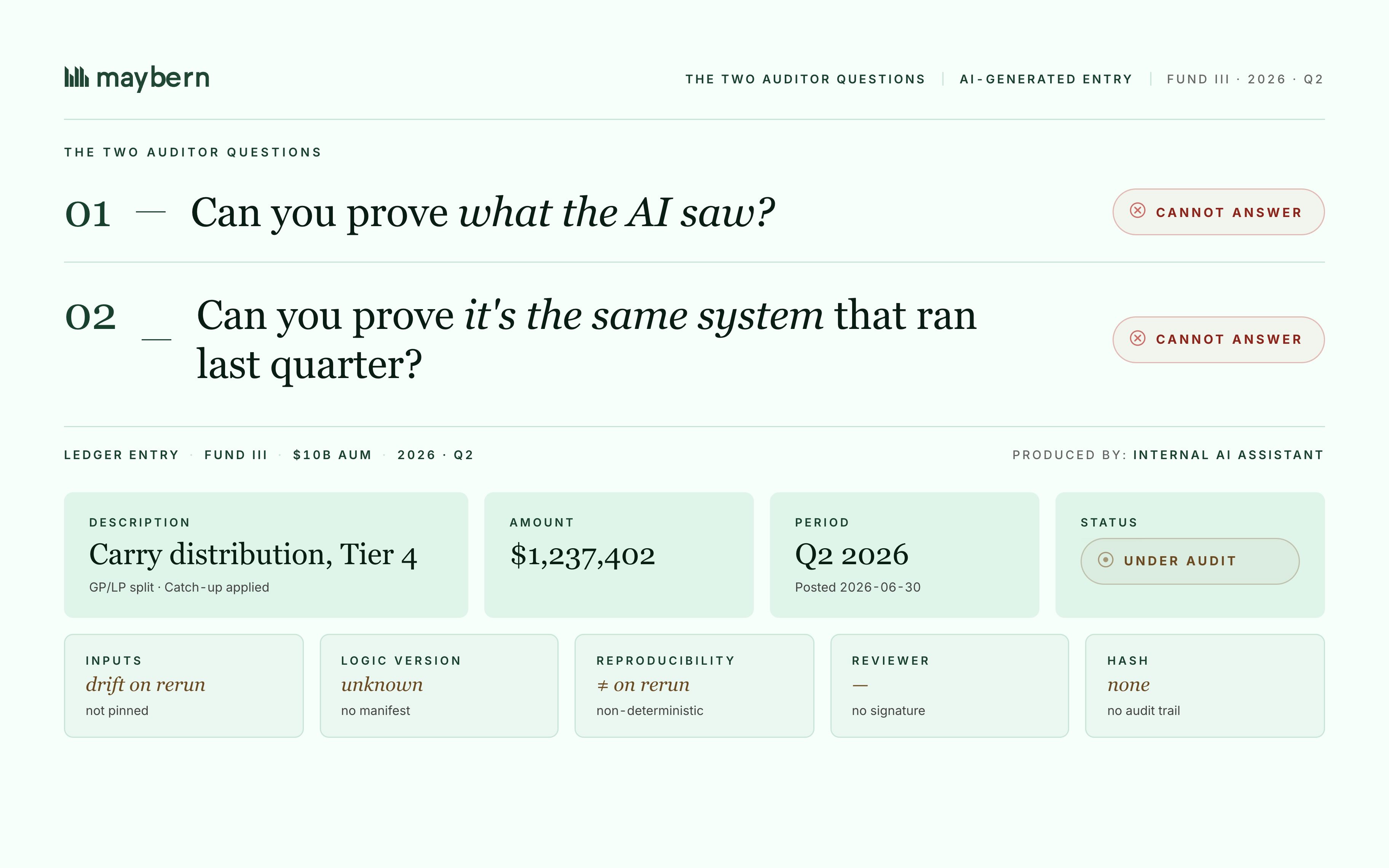

Why Internally-Built AI Fails Fund Accounting Audits